Geen blauwdruk, maar transparantie

In een industrie waar het diffuus maken van de keten regeert, wordt veel geld verdiend. Wie kan je vertrouwen? De consument is achterdochtig geworden en de boer gedesillusioneerd. Voor ons begint vertrouwen bij transparantie: wie doet er mee in de keten en wat heeft hij of zij betaald gekregen voor het werk? Je kunt dan kritische vragen stellen. Ook als koffiedrinker. In plaats van de complexiteit versimpelen in universele modellen, stimuleren wij de kritische consument in iedereen.

Op onze website bieden we een transparante prijsopbouw voor elke koffie. Hierbij gebruiken we data die direct van onze partners komt om te laten zien hoe de waarde over de keten is verdeeld. Wij vertrouwen erop dat onze partners zelf het beste kunnen definiëren wat een eerlijke prijs is in hun context, gebaseerd op hun eigen inzicht in kosten en behoeften. Dat is voor ons het vertrekpunt van elk prijsgesprek. Van daaruit gaan we de dialoog aan, stellen we vragen en schaven we samen bij om te garanderen dat onze betalingen de kosten dekken en een duurzame marge ondersteunen.

Voor ons is specialty coffee niet alleen een kwestie van smaak; het is een instrument om de verdeling van waarde actief te hervormen. Op deze manier beweeg je weg van alleen de ethische consument, en bereik je ook een bredere markt. Je geeft de boer ook de tools om te kiezen welke kwaliteit te produceren, en welk marktsegment goed bij hem of haar past.

Benchmark: Vertrouwen

Om dit concreet te maken, delen we voor elke koffie in de blend de prijsopbouw, samen met de productiegegevens die onze partners aanleveren. Deze visualisaties laten zien hoe de waarde over de keten is verdeeld en hoe onze prijsbeslissingen direct samenhangen met de realiteit bij de bron. Het kwantificeren van vertrouwen is een uitdaging, maar wij maken het tastbaar door de openheid en de verantwoordelijkheid binnen onze waardeketen aan te tonen. Door een breed scala aan informatie van onze partners te delen, bieden we meer dan alleen bewijslast; we tonen een gezamenlijke toewijding aan ieder individu in de keten. Zo zorgen we ervoor dat niemand achterblijft.

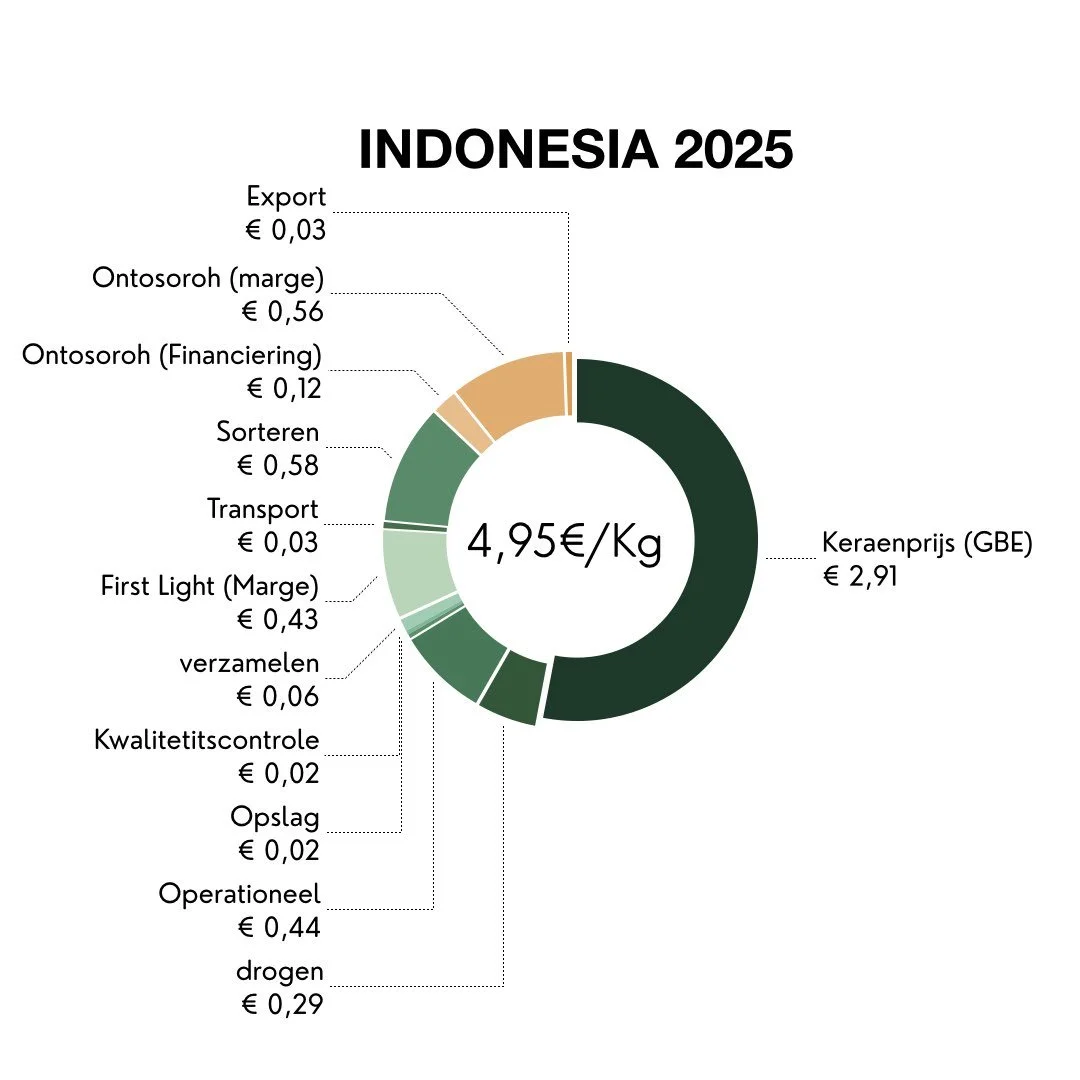

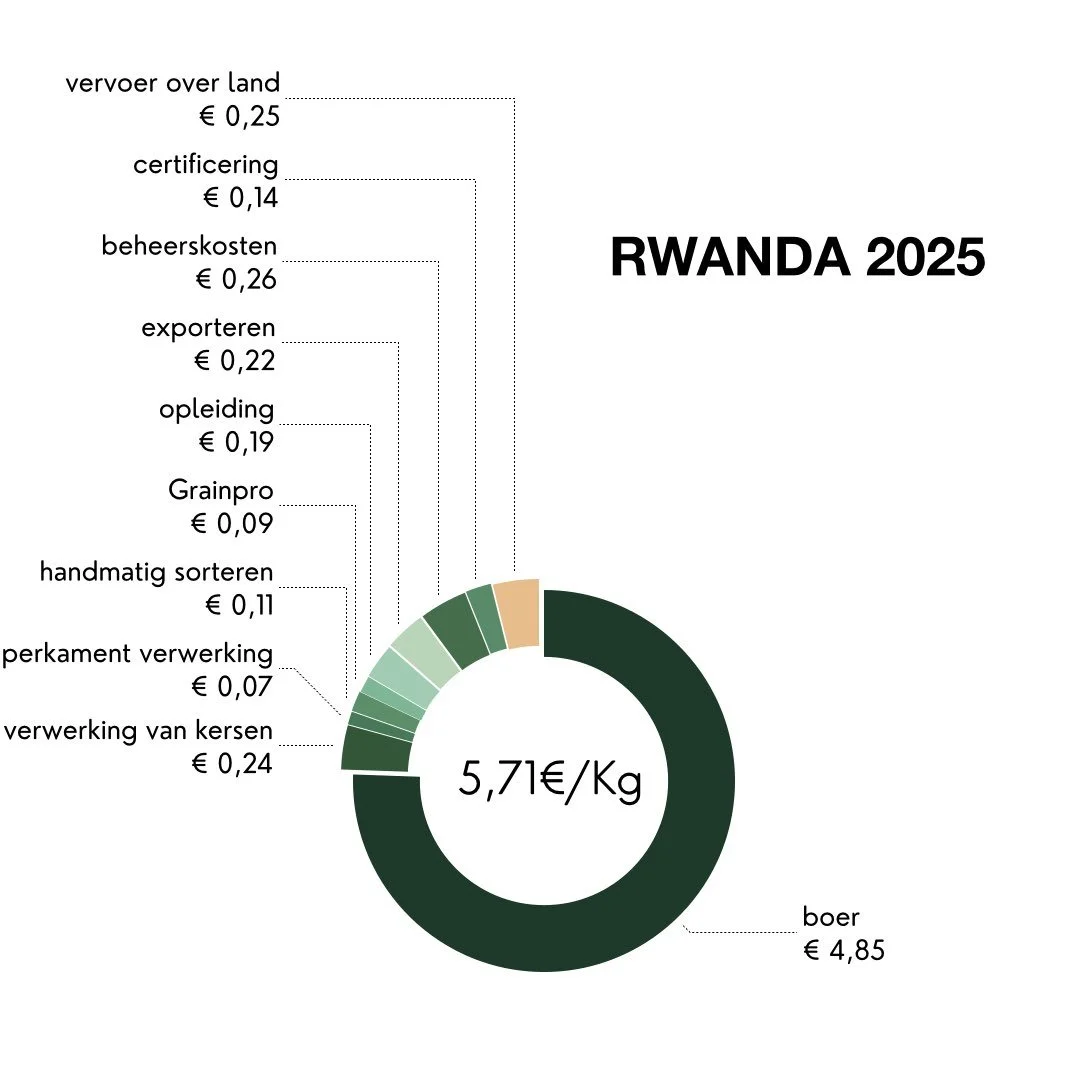

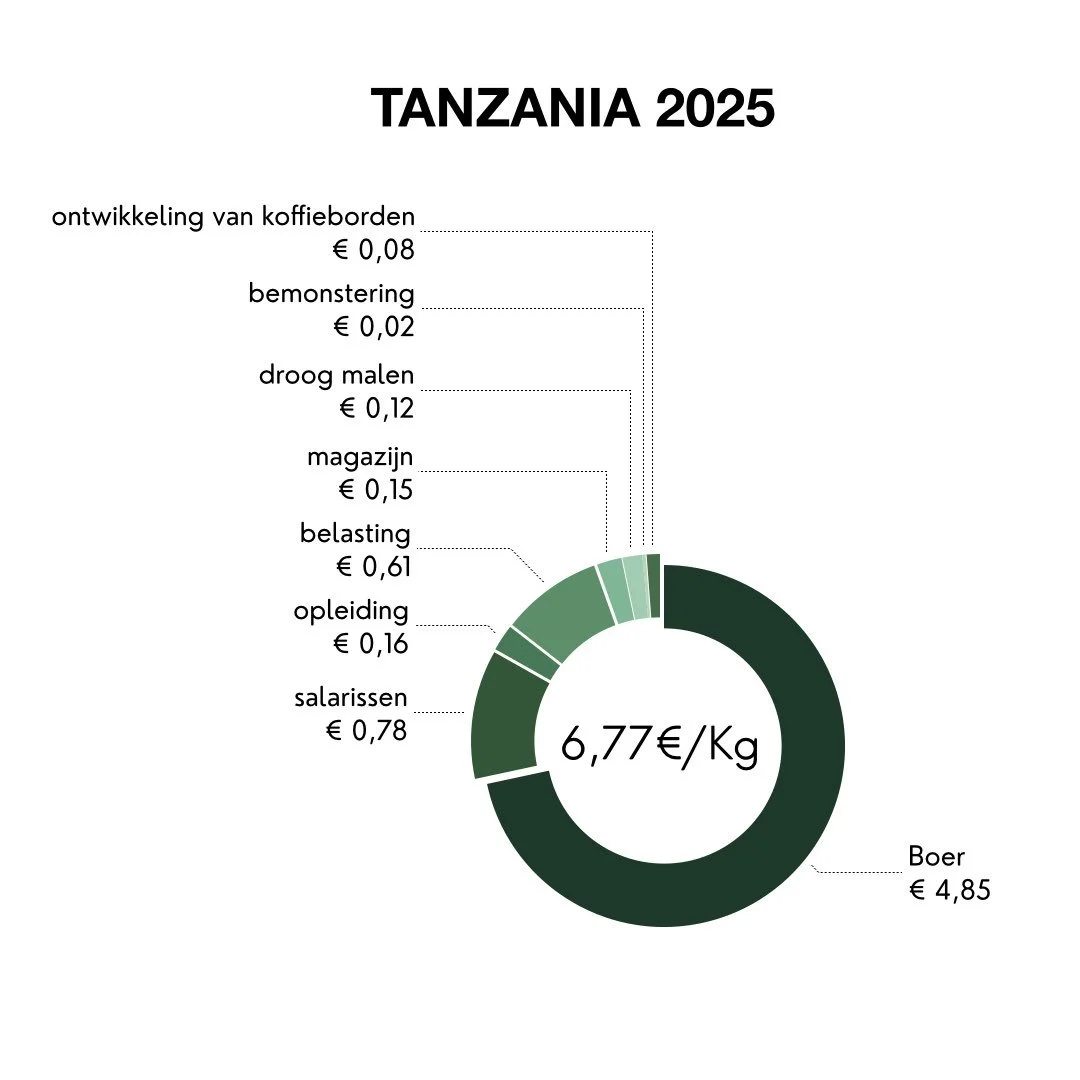

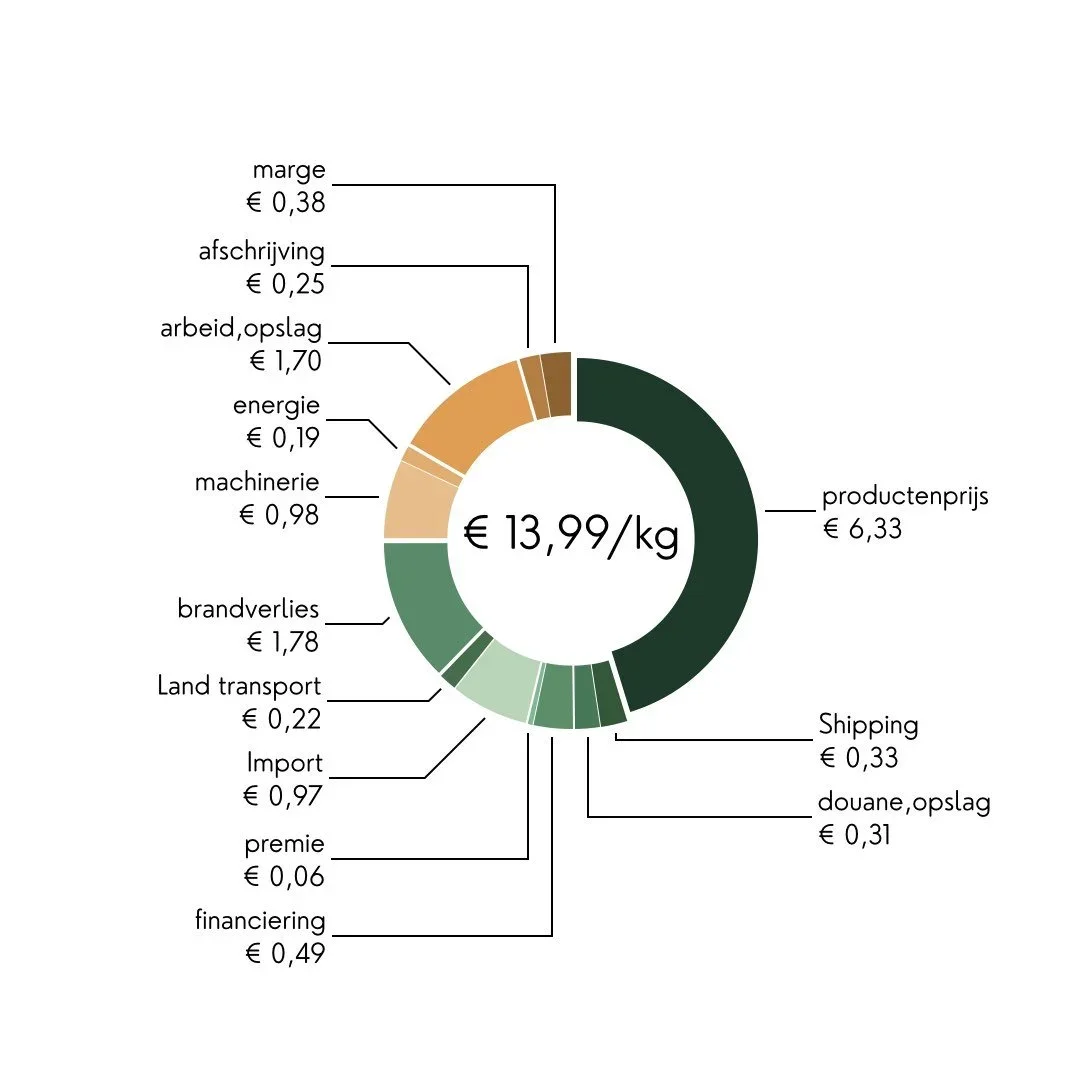

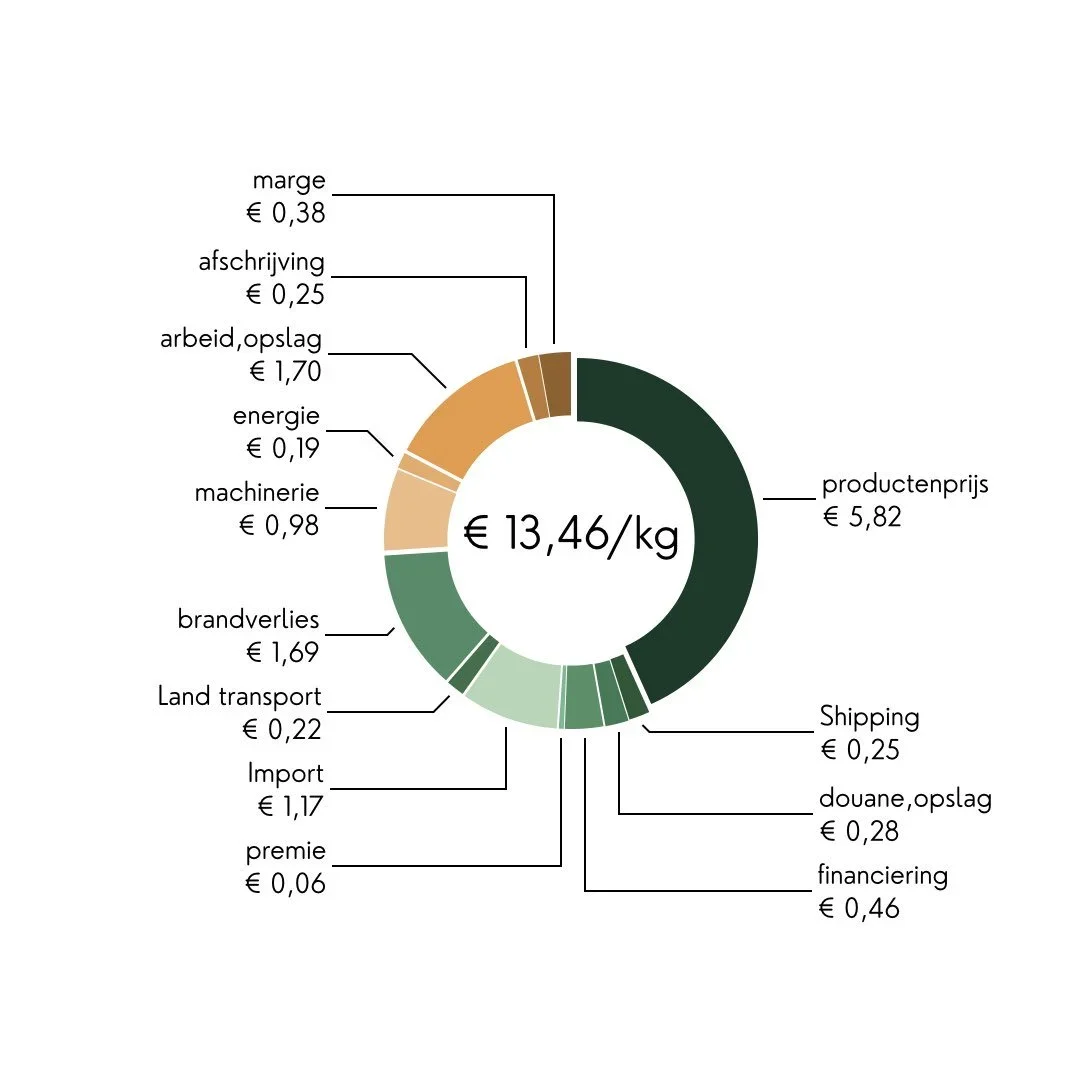

PRIJSWIELEN bieden een transparant overzicht van wie precies welk bedrag ontvangt voor elke kilogram koffie. Deze data zijn gebaseerd op actuele kosten en worden jaarlijks bijgesteld om de veranderende economische realiteit van onze boeren te weerspiegelen. Zo garanderen we dat onze prijsstelling altijd nauwkeurig en rechtvaardig blijft.

Stap 1: Wie leveren er koffie aan de Gemeente Amsterdam?

Stap 2: Van boerderij tot aan het schip

Stap 3: Van het schip tot aan Selecta Netherlands

Benchmark: Kwaliteitssegmentatie in de markt

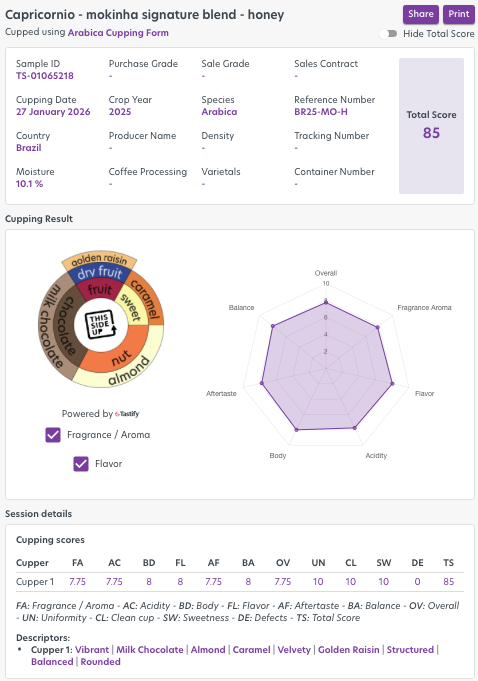

Wat is de markt bereid te betalen voor een bepaalde kwaliteit? Dit begint bij het uitsorteren van kwaliteiten. Koffie is niet “gewoon koffie” zoals vele grote partijen ons willen doen geloven. We gebruiken hiervoor de standaarden van de Specialty Coffee Association en This Side Up heeft een in house kwaliteitslab. Alle koffies worden beoordeeld op cup score wat de aroma’s, smaken, mondgevoel en meer meeneemt. Iedere koffie krijgt zo een eigen rapport. Dit rapport wordt ook gedeeld met de producenten, en er is altijd een gesprek waarin er wordt teruggekoppeld. Dit gaat dan niet alleen over de feitelijke score, maar ook hoe de markt het product heeft ervaren in termen van consistentie en bruikbaarheid. Sommige koffies zijn bijvoorbeeld erg goed, maar allicht te uitgesproken voor veel consumenten.

Dit alles gebeurt in open communicatie. Onze rapporten zijn publiek inzichtelijk. Het grote voordeel van werken met de standaarden van de Specialty Coffee Association is dat deze overal ter wereld identiek zijn. We praten dezelfde taal, of het nu Indonesië, Rwanda of Brazilië betreft.

De basisaanname achter kwaliteit, is dat een hogere score meer arbeid met zich meebrengt, en ook een betere betaling met zich meebrengt. Dit kun je ook omdraaien: als een producent een klein areaal heeft en meer geld nodig heeft voor zijn of haar behoeften, is investeren in betere kwaliteiten een logische keuze. Het is dan aan This Side Up en de producent om hier samen een goede markt voor te vinden.

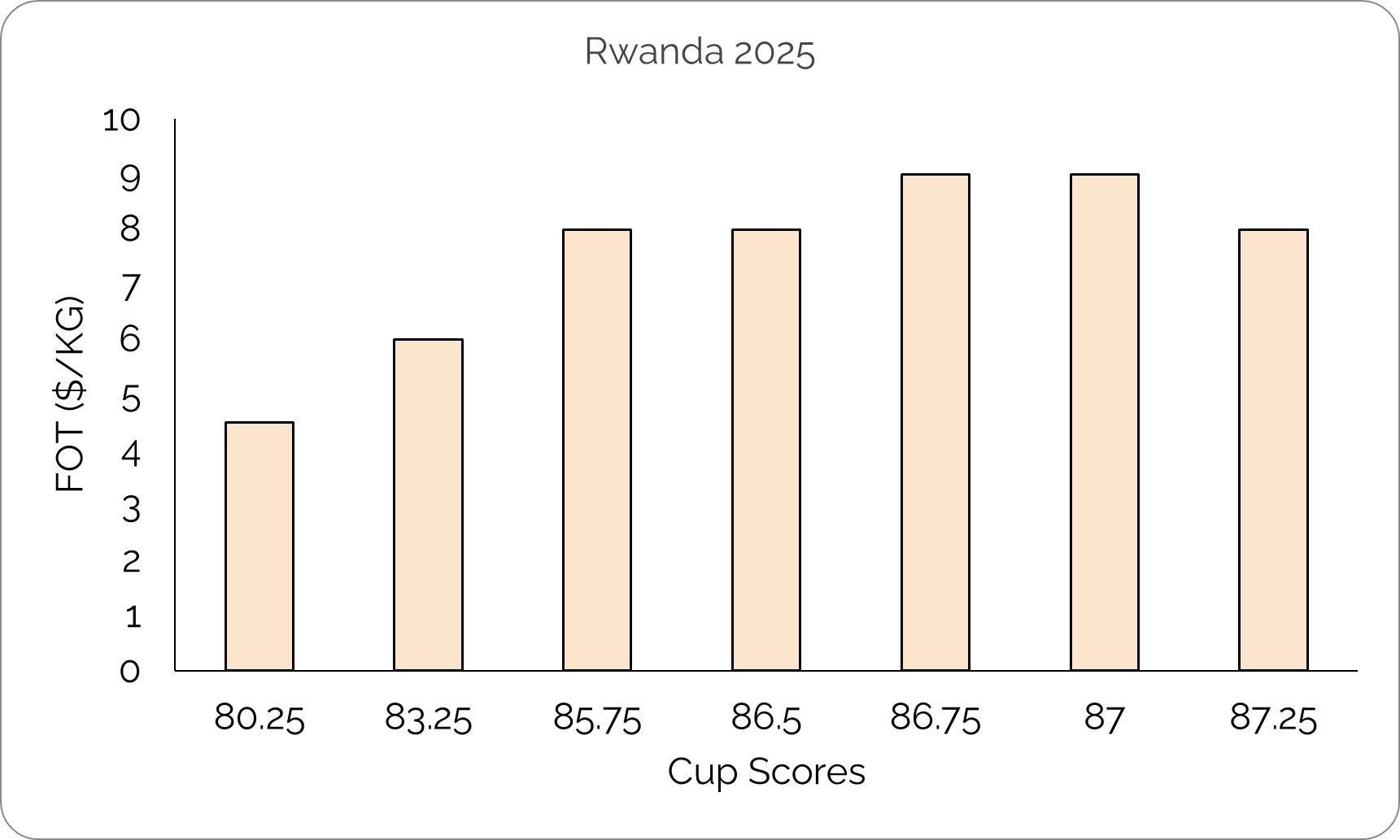

Wat heeft This Side Up betaald per kwaliteit?

Hier tonen we, met Rwanda als voorbeeld, het spectrum aan kwaliteiten dat we inkopen op basis van de cup score. Elke kwaliteitsklasse heeft een eigen prijs, die de inspanning weerspiegelt die nodig is voor de productie. Een lager gesegmenteerde specialty coffee vereist vanuit de productie minder intensieve verwerking dan koffies met een hogere score.

In 2026 zullen de prijzen voor alle kwaliteiten iets hoger liggen. Dit is noodzakelijk om aan te sluiten bij de inflatie en de lokale marktprijzen, en om de productiekosten te dekken. Elk jaar worden deze variabelen zorgvuldig gewogen voordat de prijs definitief wordt vastgesteld.

Een kleine kanttekening bij het laatste datapunt voor Rwanda: dit betreft een koffie met een hoge score, maar een lagere prijs. Dit is mogelijk dankzij de schaalgrootte waarop de coöperatie deze koffie op centraal niveau verwerkt; door de volumes kan de coöperatie (het wasstation) het zich veroorloven deze koffie tegen een iets lagere prijs aan te bieden.

Hier tonen we de prijzen voor verschillende kwaliteiten.

Hier tonen we de prijzen voor verschillende kwaliteiten.

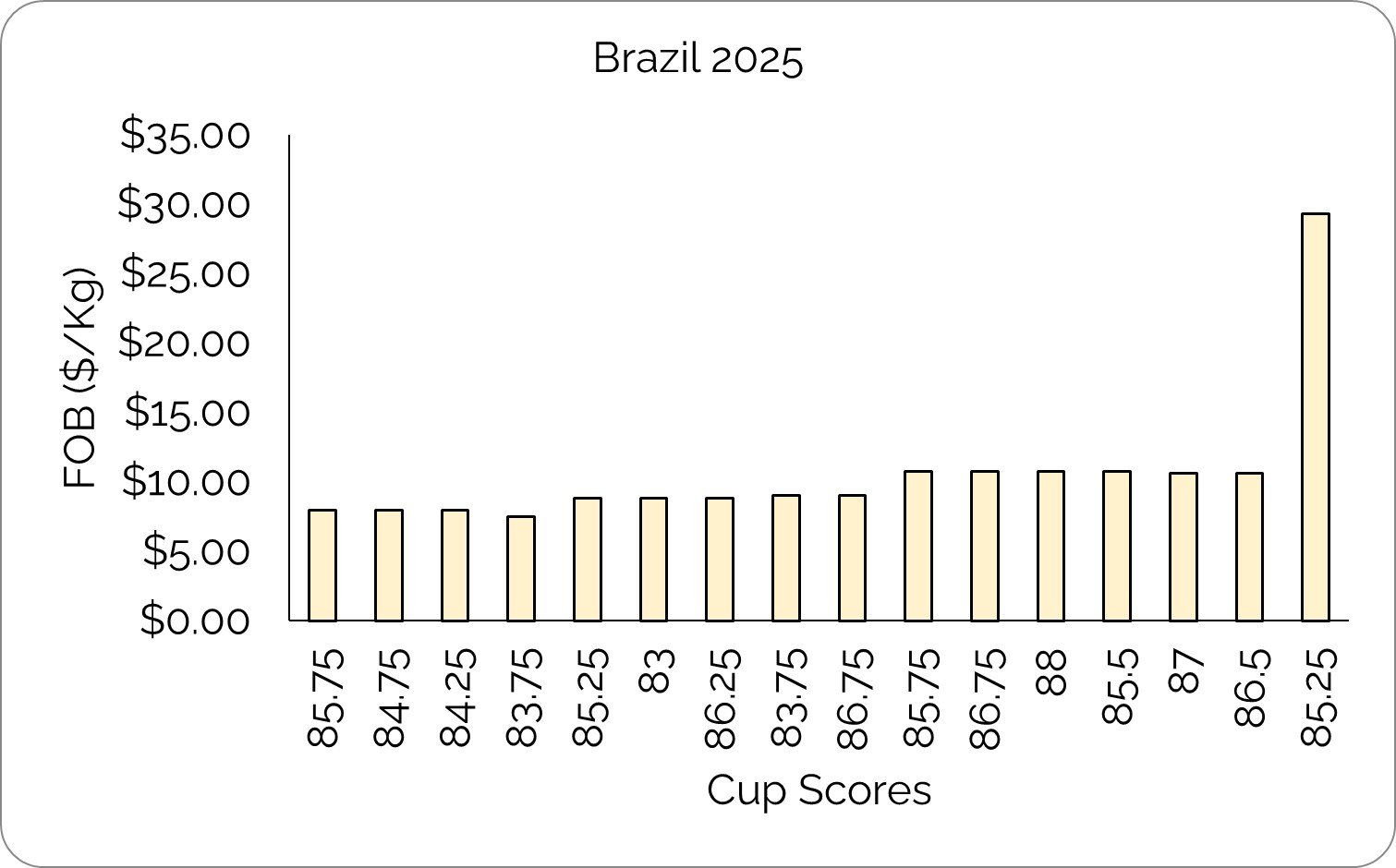

Ons portfolio in Brazilië is onderverdeeld in drie hoofdsegmenten:

Blends: Deze worden samengesteld op basis van een specifiek gewenst smaakprofiel. Meestal hebben deze een score tussen de 83 en 85 punten. Dit segment vormt de basis van ons portfolio — het zijn de koffies die voor zowel boer, exporteur, importeur en brander die 'de rekeningen betalen'.

Single Farm of Coop Lots: Koffies die afkomstig zijn van één enkel landgoed of van een specifieke groep, zoals onze Women’s Lots.

Experimental Lots: De exclusieve koffies die een hoge prijs opbrengen, maar die ook een aanzienlijke inspanning en expertise vereisen tijdens het productieproces.

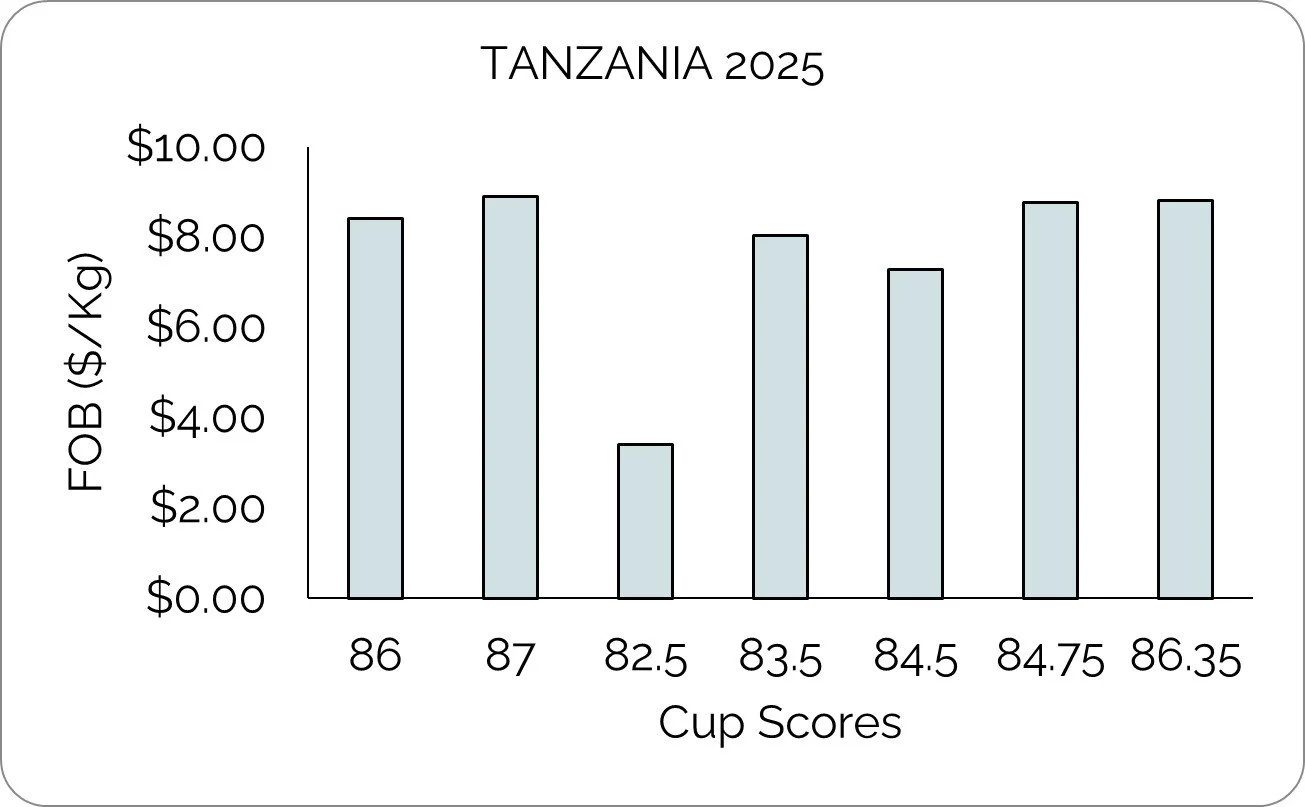

Ons portfolio in Tanzania is wat betreft de verhouding tussen kwaliteit en prijs zeer overzichtelijk. De koffies met een hogere score zijn iets hoger geprijsd dan de lagere segmenten binnen de specialty coffee.

Vanaf 2025 zijn we begonnen met het inkopen van meer “gradaties” naast de standaard A1-kwaliteit. Dit vergroot de mogelijkheden voor diversificatie en vermindert de druk op de boer om uitsluitend lots met een extreem hoge score te produceren.

Hier tonen we de prijzen voor verschillende kwaliteiten.

Hier tonen we de prijzen voor verschillende kwaliteiten.

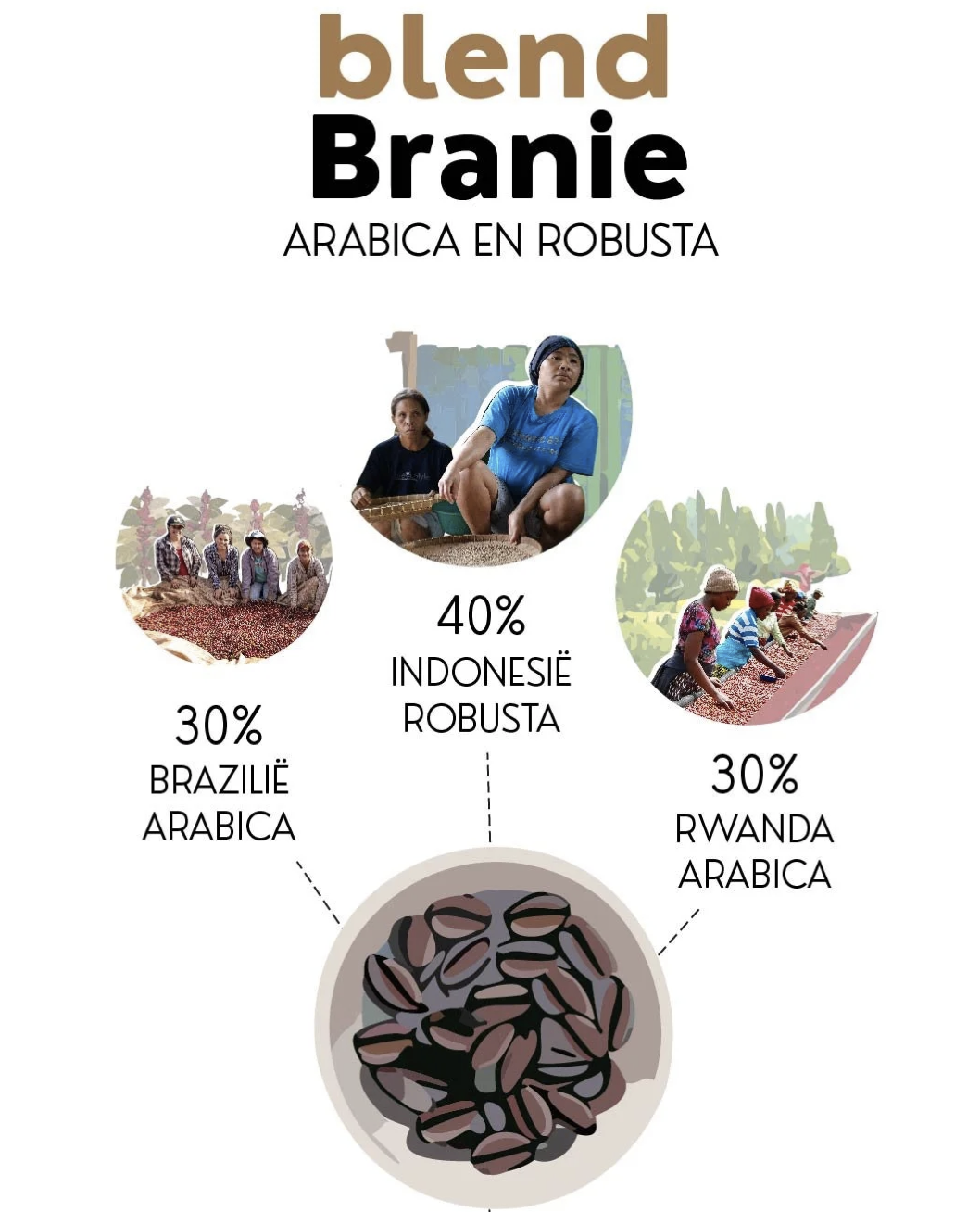

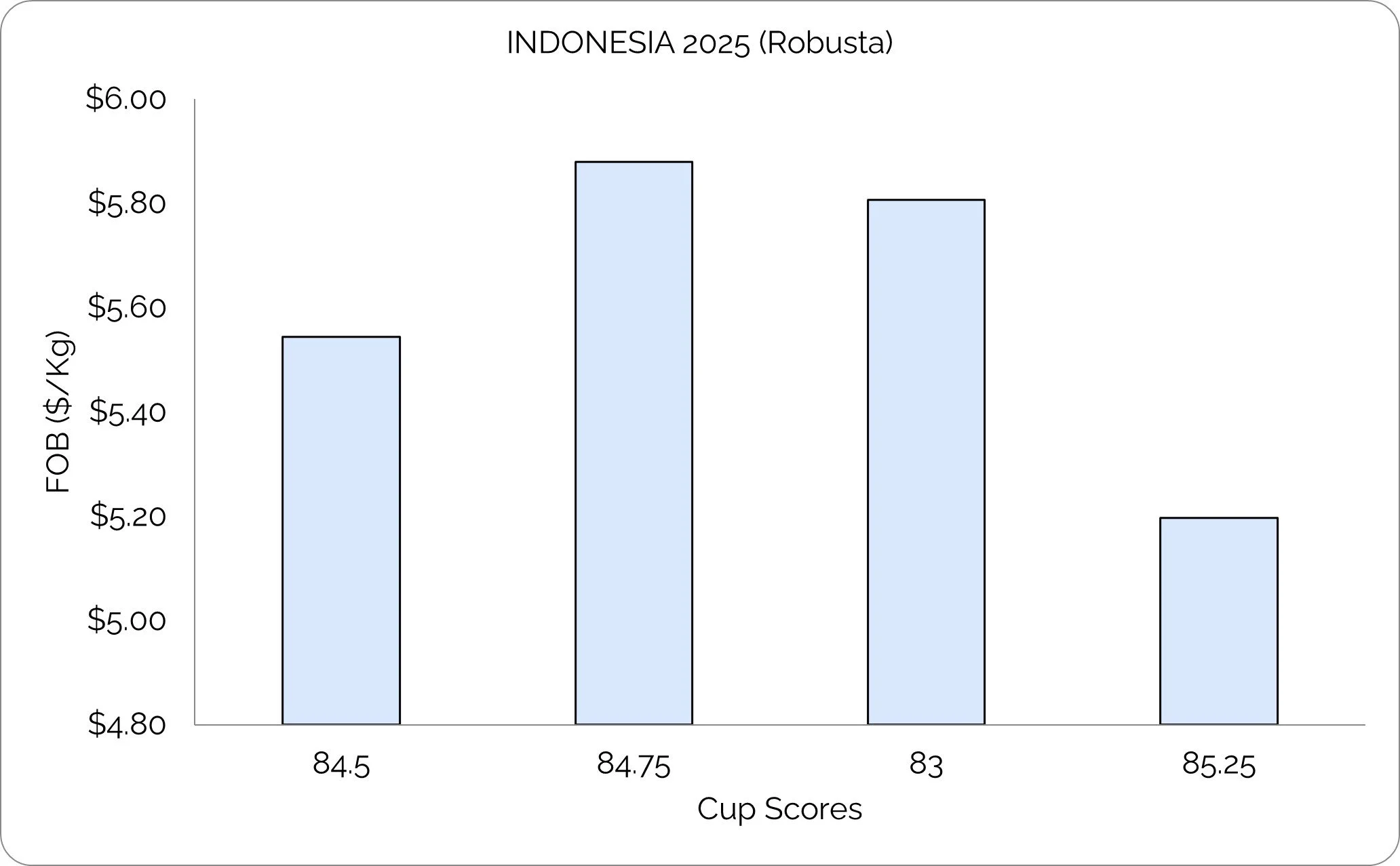

Uit Indonesië kopen we zowel Arabica als Robusta in. De Robusta stellen we voor in blends voor net dat beetje extra 'kick'. We werken samen met groepen jongeren op de eilanden Flores en Java, van wie we de koffie contracteren. Een mix van deze twee regio's vormt de basis voor Branie.

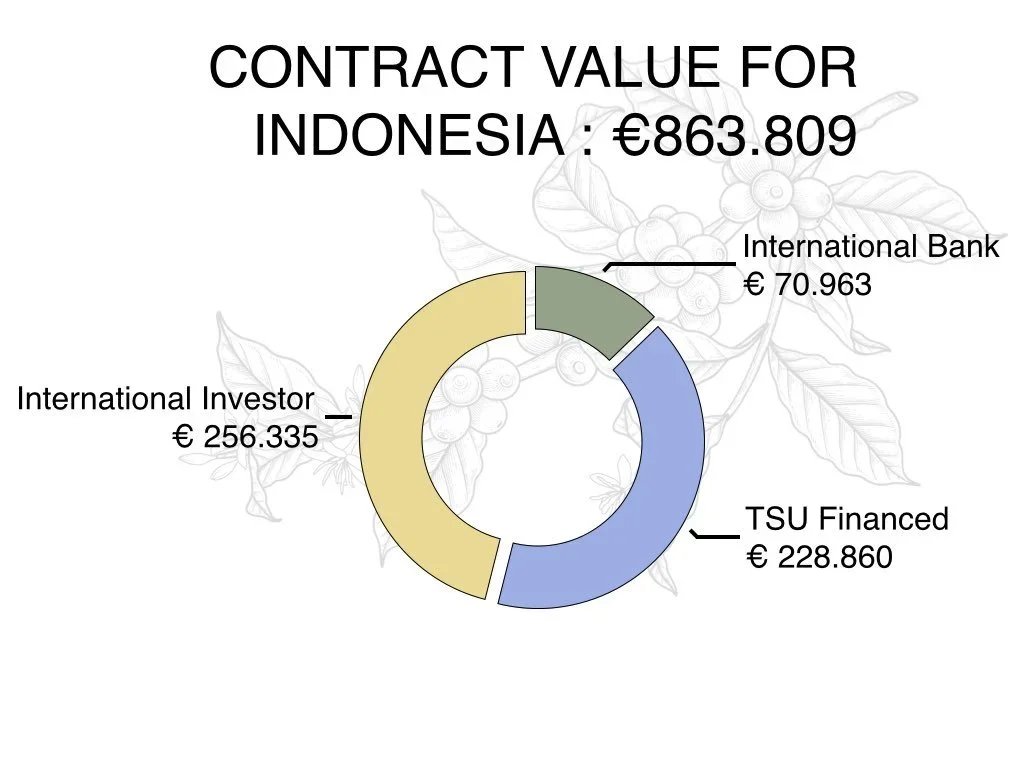

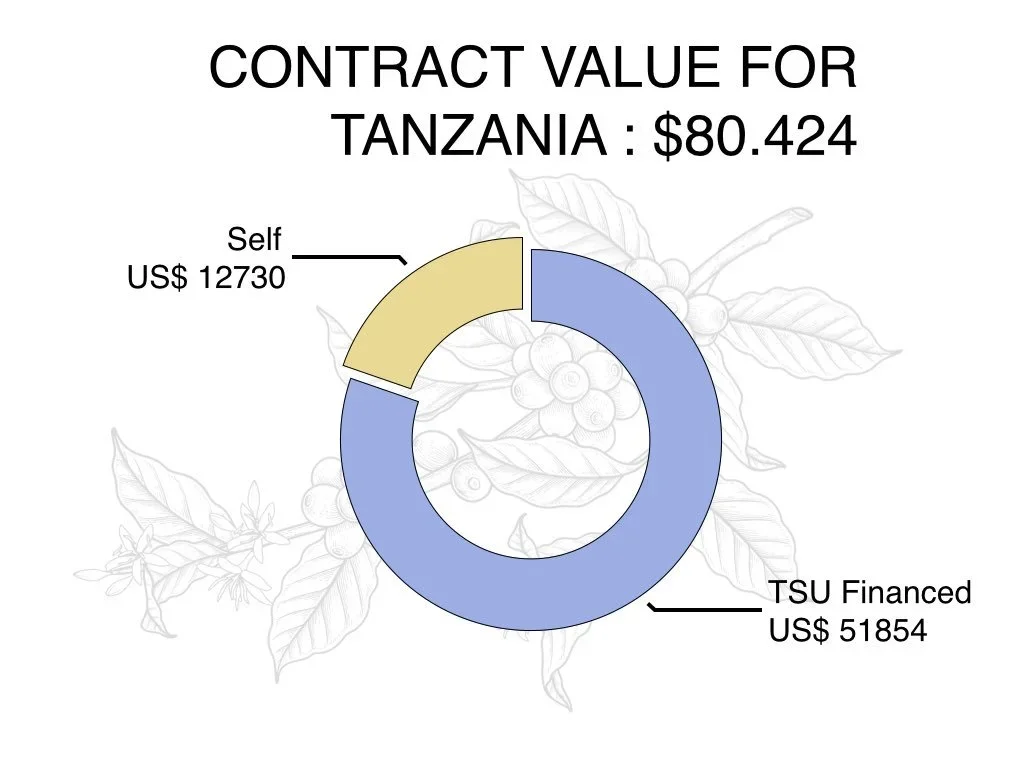

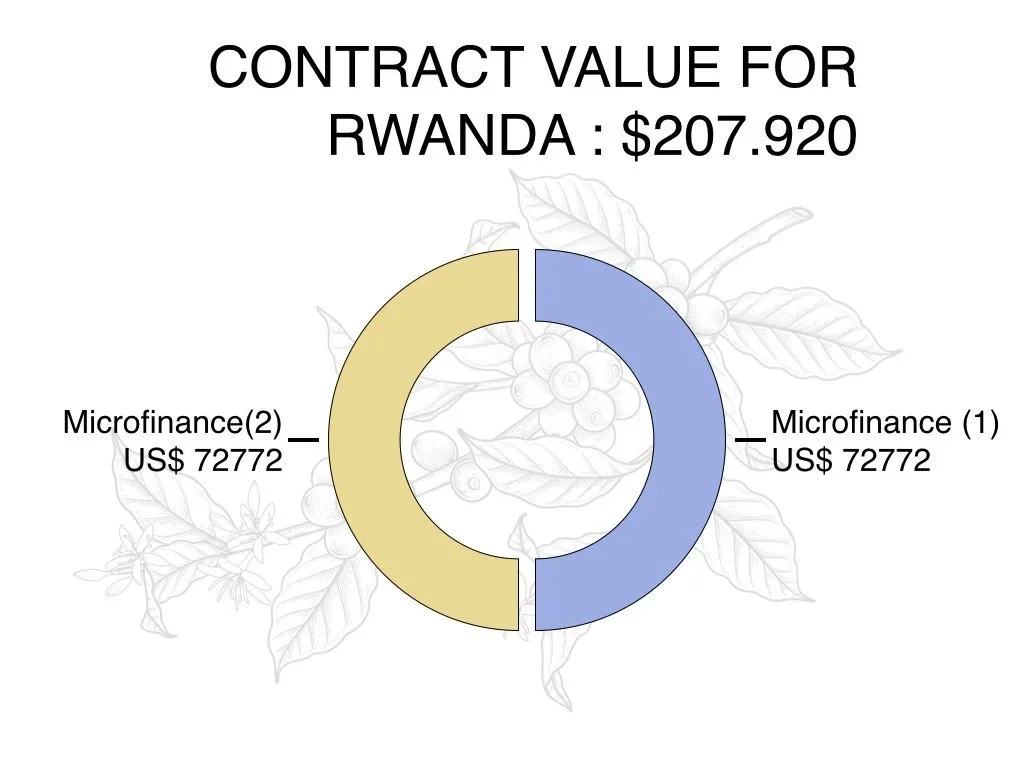

Benchmark: Financieringsbehoefte

Om koffie van hoge kwaliteit te kunnen produceren, is kapitaal nodig. This Side Up beschikt over samenwerkingen met financiële instellingen maar ook het gebruik van eigen kapitaal om hierin te voorzien. Voor de Amsterdam-blend hebben de partners uit Rwanda, Tanzania en Indonesië om voorfinanciering verzocht. Dit betreft de coöperatie (met eigen wasstation) in Rwanda, de exporteur in Wanza (welke een aantal boerengroepen vertegenwoordigt) en de exporteur in Indonesië, welke ook verschillende boerengroepen van verschillende eilanden in Indonesië vertegenwoordigt. Zij zetten de financiering weer door naar hun lokale partners, om zo vroeg in de oogst de koffies al te verzekeren en de boeren rust te geven. De partners in Brazilië hebben dit via hun eigen netwerk geregeld. In de grafiek maken we inzichtelijk welk deel van de contractwaarde (%) we hebben voorgefinancierd en hoeveel maanden voorafgaand aan de export dit heeft plaatsgevonden.

In totaal is 64% van de contractwaarde van het contract met exporteur Ontosoroh voorgefinancierd.

80% van de contractwaarde met exporteur Wanza is voorgefinancierd.

Het This Side Up contract is gebruikt als garantie om 70% van de voorfinanciering te organiseren.